Almost 90% of Indian investors stop their SIPs before the three-year period is up. That’s barely enough time for investments to show the power of compounding.

This behaviour repeats itself during every market correction. A 10% dip usually triggers panic across investor groups, with the same question flooding financial forums: “Should I stop my SIP?” What’s particularly troubling is that these same investors later claim SIPs don’t deliver results.

But here’s the thing: SIPs work brilliantly. The problem lies in execution, not the instrument itself. Let’s understand what’s actually going wrong and how you can avoid the same traps.

Most people start SIPs because their friend is doing it, or some Instagram reel made it look easy. They will invest ₹5,000 monthly without knowing whether they are saving for retirement in 25 years or a car down payment in 3 years.

This matters more than you think. Your goal decides which funds you pick, how long you stay invested, and whether you should even be in equity at all.

There’s always a reason to delay. “I’ll start later—after the promotion, after the loan, after things settle.”

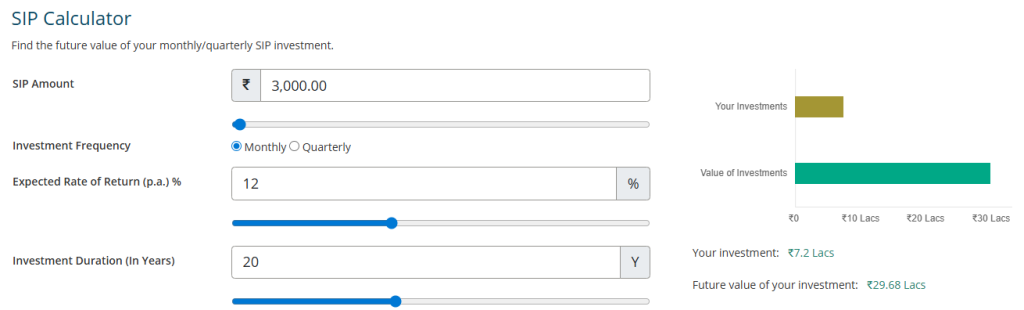

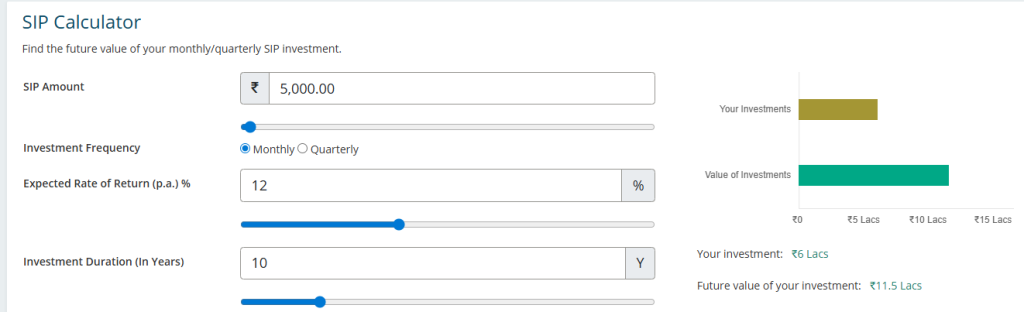

Meanwhile, the only thing happening here is you are losing the precious time. Starting a ₹3,000 SIP at 25 beats starting a ₹10,000 SIP at 35. The math is brutal but simple.

Here’s an example below:

If you invest ₹3000 from the age of 25 to 45, it will result in ~29 lakhs.

However, investing ₹5000 from the age of 35 to 45 results in only ~11 lakhs, which is a loss of almost 18 lakhs.

The truth is, the market doesn’t care about your perfect moment, and every month you delay costs you more than you realise.

This behaviour destroys long-term returns more than any other mistake. For instance, a 15% market correction nearly always results in a surge of investor SIP pauses.

The entire point of SIPs is rupee cost averaging. Lower prices let you buy more units; higher prices mean you buy less. Pause your SIP during a fall, and you’ve basically thrown away its biggest advantage. The investors who got the most benefits of SIPs were the ones who kept investing through 2008, 2020, and every correction in between.

“Markets are at all-time highs. Better to wait for a correction.”

This statement has been repeated at Sensex levels of 40,000, 50,000, and 60,000. Those who waited missed significant appreciation while searching for the perfect entry point that never materialised.

Dividends in mutual funds aren’t bonus payouts. The fund’s literally taking money from your investment, paying it out, and then taxing it. Meanwhile, growth plans reinvest everything and let compounding work its magic. Over 10-15 years, the difference is staggering, often 30-40% lower returns with dividend plans.

IT funds looked brilliant in 2021. Pharma funds were the darlings during COVID. Everyone wanted a piece of the EV revolution in 2022. Remember PSU funds in early 2024?

Sectoral and thematic funds are incredibly volatile. They’ll give you returns when their sector’s in favour and destroy your portfolio when it’s not. Most investors don’t have the patience or knowledge to rotate between sectors at the right time.

It is better to stick to diversified equity funds. Large-cap, flexi-cap, or multi-cap funds should form the backbone of your portfolio.

SIP investing isn’t a one-time decision. Income levels change, financial goals evolve, and market conditions shift. A ₹5,000 monthly commitment from five years ago should logically increase as earning capacity grows.

Most investors never adjust their SIP amounts. They expect wealth to grow proportionally while income has potentially doubled. If lifestyle expenses increase annually, investment contributions should follow the same trajectory.

Establish SMART goals for every SIP. Replace “save for retirement” with “accumulate ₹5 crore by age 55 for retirement.”

Implement automatic step-up SIPs with 10-15% annual increases. Your investment grows alongside income without requiring manual intervention or annual reminder tasks.

Build a core portfolio with diversified equity funds. Large-cap, flexi-cap, and multi-cap funds gives you adequate diversification and reduce portfolio-specific risk.

Run calculations before committing. SIP calculators show realistic projections based on historical returns. This sets appropriate expectations and prevents disappointment when short-term returns fluctuate, which they will.

The perfect moment to start an SIP was a decade ago. The next best moment is today—if you make sure to avoid these seven pitfalls going ahead.

Open Free Demat Account!

In just a few minutes, Simply provide some basic personal details, to get started.

About | Research | Pricing | Upcoming IPOs | Blog | Become a Partner | RMS Policy | Privacy Policy

Fund Transfer for Trading | Fund Transfer for DP | Client Back office/DP Login | Partner Login | Buy-Back | Margin Calculation | Re-KYC | Downloads | Platform | Loans

CIN - U65921WB1994PLC217071 | SEBI Registration No. INZ000169130 | DP SEBI Reg ID : IN-DP-533-2020 | CDSL : 1234500 | NSDL : IN303591 | Member ID`s : NSE - 08334, BSE - 912, MSEI - 18300, ICEX - 1133, MCX - 56415, NCDEX - 1286 | AMFI : ARN-12417 | Research Analyst : INH000000206

Trinity, 226/1, A.J.C. Bose Road, 7th Floor, Kolkata - 700 020, India.

**Investments in securities market are subject to market risks, read all the related documents carefully before investing.