Canara Bank’s Q2 FY26 performance delivered numbers that demonstrate the public sector lender is executing well on its transformation agenda. Net profit climbed 18.93% year-on-year to ₹4,774 crore, while global business expanded 13.55% to ₹26,78,963 crore, outpacing the guidance provided for the full year.

For investors evaluating India’s banking sector, these results raise questions about whether Canara Bank can maintain this trajectory while preserving asset quality and margins in an increasingly competitive environment.

Canara Bank operates as one of India’s leading public sector banks with a heritage spanning over a century. The bank maintains a significant presence across urban, semi-urban, and rural markets with 9,948 domestic branches as of September 2025, alongside four international branches in key financial centers including New York, London, and DIFC Dubai.

The institution has positioned itself across retail, MSME, agriculture, and corporate segments, with particular emphasis on priority sector lending, where it has exceeded all mandated regulatory targets.

Global deposits grew 13.40% year-on-year to ₹15,27,922 crore, while global advances increased 13.74% to ₹11,51,041 crore. The credit-deposit ratio stood at 75.33%, reflecting disciplined balance sheet management.

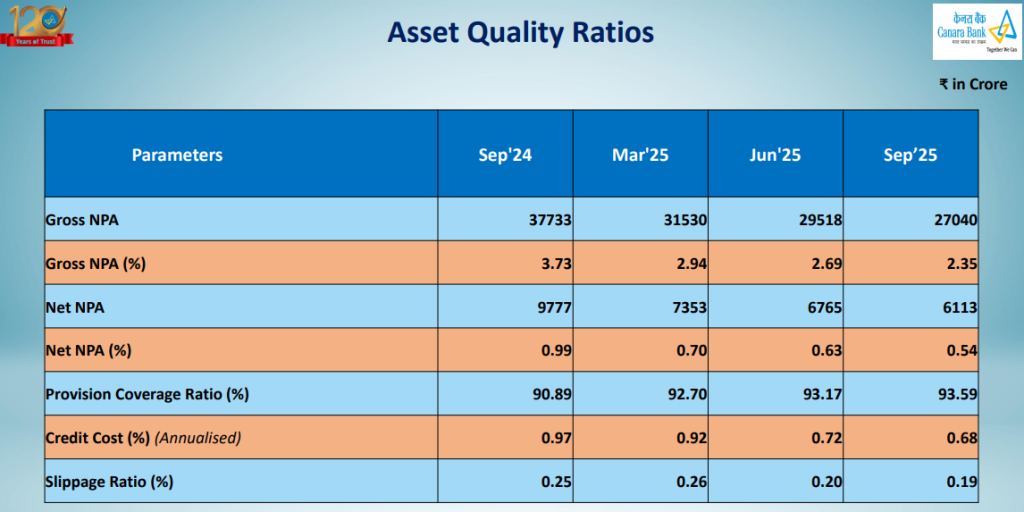

Source: Canara Bank Investor Presentation

Operating profit expanded 12.20% to ₹8,588 crore, demonstrating operational efficiency despite margin pressures. Net Interest Margin declined to 2.52% on an annualised basis from 2.88% in the corresponding quarter last year, primarily driven by higher cost of funds amid competitive deposit mobilisation.

The bank’s focus on retail, agriculture, and MSME (RAM) segments showed strong results, with RAM credit reaching ₹6,71,141 crore, a 16.94% year-on-year increase. Retail credit surged 29.11% to ₹2,51,190 crore, with housing loans growing 15.25% and vehicle loans expanding 25.58%.

CASA deposits to domestic deposits stood at 30.69%, below the bank’s guidance of 32% for March 2026, indicating room for improvement in low-cost deposit mobilisation. Current account deposits grew an impressive 62.84% year-on-year, though this came off a lower base.

The most compelling aspect of Canara Bank’s Q2 performance lies in asset quality improvement. Gross NPA ratio declined 138 basis points year-on-year to 2.35%, while Net NPA ratio compressed to 0.54% from 0.99%.

Provision Coverage Ratio expanded substantially to 93.59%, up 270 basis points, providing significant comfort on balance sheet strength. Credit cost improved to 0.68% on an annualized basis, down 29 basis points year-on-year.

Special Mention Accounts worth ₹5 crore and above declined to ₹3,862 crore, representing just 0.34% of gross advances—a material improvement from 1.15% in the corresponding quarter last year. The slippage ratio of 0.76% remained well below the bank’s full-year guidance of 0.90%.

Cash recoveries, including written-off accounts, totalled ₹2,555 crore during the quarter, demonstrating effective recovery mechanisms. The bank resolved accounts worth ₹442 crore through various NCLT processes during the first half of FY26.

Also read: Bharat Electronics Q2 FY26 Results: 26% Revenue Growth; Is This Defence Stock’s Rally Sustainable?

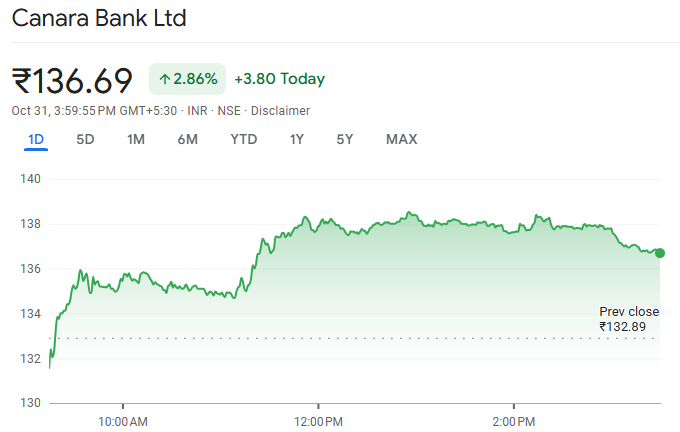

Investors greeted the results with optimism, pushing Canara Bank’s share price to over 7% in the last week and more than 40% in the last 6 months.

Source: Google Finance

The market response highlights confidence in management’s conservative growth trajectory and asset quality improvements.

For investors evaluating public sector banking exposure, Canara Bank’s Q2 FY26 results demonstrate that the lender is successfully navigating the transition toward higher retail and MSME exposure while strengthening asset quality metrics.

The question for investors is whether current valuations adequately reflect the risk-reward profile given the improving fundamentals, or whether execution challenges on deposit mobilization and margin compression present headwinds to the growth narrative.

Analysis based on Canara Bank Q2 FY26 investor presentation. Banking sector performance subject to interest rate movements, credit demand cycles, and regulatory changes. This represents analytical perspective, not investment advice.

Click here for more stock market blogs.

For more insightful articles and updates, follow us on Facebook and Instagram.

Open Free Demat Account!

In just a few minutes, Simply provide some basic personal details, to get started.

About | Research | Pricing | Upcoming IPOs | Blog | Become a Partner | RMS Policy | Privacy Policy

Fund Transfer for Trading | Fund Transfer for DP | Client Back office/DP Login | Partner Login | Buy-Back | Margin Calculation | Re-KYC | Downloads | Platform | Loans

CIN - U65921WB1994PLC217071 | SEBI Registration No. INZ000169130 | DP SEBI Reg ID : IN-DP-533-2020 | CDSL : 1234500 | NSDL : IN303591 | Member ID`s : NSE - 08334, BSE - 912, MSEI - 18300, ICEX - 1133, MCX - 56415, NCDEX - 1286 | AMFI : ARN-12417 | Research Analyst : INH000000206

Trinity, 226/1, A.J.C. Bose Road, 7th Floor, Kolkata - 700 020, India.

**Investments in securities market are subject to market risks, read all the related documents carefully before investing.