Investment choices shape the path to financial goals, especially in a dynamic year like 2025. India’s total demat account base grew robustly, crossing 20 crore accounts by mid-2025. Systematic Investment Plans (SIPs) and Lump-Sum investments are two popular methods for investing in mutual funds, each with distinct advantages and risks. As market volatility and economic uncertainties persist this year, investors must understand which approach aligns best with their risk appetite, income pattern, and financial objectives.

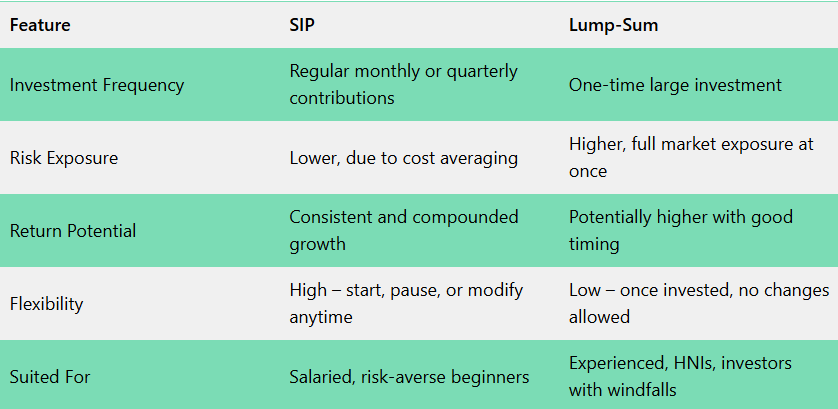

A Systematic Investment Plan (SIP) allows investors to invest fixed amounts periodically, usually monthly, into mutual funds. Think of it as setting your investments on autopilot, where a predetermined amount gets deducted from your account and invested regardless of what markets are doing at that moment.

This method offers several benefits:

However, SIPs may underperform during sustained market rallies compared to lump-sum investments and require disciplined, regular contributions for optimal growth.

Also read: What is NAV in Mutual Funds?

Lump-Sum investing involves investing a large amount in one go. This strategy can yield higher returns if the timing coincides with market lows or bullish trends. Key advantages include:

The downside is the higher risk associated with market volatility. Poor timing can lead to losses, making it suitable primarily for experienced investors comfortable with market fluctuations.

The investment landscape in 2025 is marked by volatility and uncertain interest rate trajectories. These conditions favour a cautious investment approach. SIPs provide an advantage by spreading investments over various market cycles, thus reducing risk.

Lump-Sum investments can be rewarding if deployed during market dips but carry high timing risk in such unpredictable conditions. Experts increasingly recommend a hybrid approach leveraging SIP discipline with opportunistic lump-sum investing during market corrections.

Also read:

Combining SIPs with lump-sum investments can optimize returns while managing risk in volatile markets. Investors can maintain regular SIPs to build a steady corpus and deploy lump-sum funds during market corrections to capture higher growth. This approach balances disciplined investing with strategic market timing suited to Indian investors.

Also read: What is AUM in Mutual Funds?

Selection between SIP and lump-sum depends on:

Investors should assess these factors and consider consulting financial advisors to tailor strategies.

Choosing between SIP and lump sum depends on your financial circumstances, risk tolerance, and market conditions. SIPs offer a safer, flexible, and disciplined pathway, especially suitable in 2025’s volatile environment. Lump sum investments can deliver higher rewards but require smart timing and risk appetite. A hybrid strategy blending both options may provide the best outcome, allowing Indian investors to leverage market opportunities while cushioning volatility.

Start evaluating your financial goals and risk profile today. Consult your financial advisor to design an investment plan that maximises returns while keeping your comfort with risk in focus. With the right strategy, 2026 can be a fruitful year for building wealth through mutual fund investments.

This guide provides educational information about investment strategies. Past performance doesn’t guarantee future results.

Click here for more stock market blogs.

For more insightful articles and updates, follow us on Facebook and Instagram.

Open Free Demat Account!

In just a few minutes, Simply provide some basic personal details, to get started.

About | Research | Pricing | Upcoming IPOs | Blog | Become a Partner | RMS Policy | Privacy Policy

Fund Transfer for Trading | Fund Transfer for DP | Client Back office/DP Login | Partner Login | Buy-Back | Margin Calculation | Re-KYC | Downloads | Platform | Loans

CIN - U65921WB1994PLC217071 | SEBI Registration No. INZ000169130 | DP SEBI Reg ID : IN-DP-533-2020 | CDSL : 1234500 | NSDL : IN303591 | Member ID`s : NSE - 08334, BSE - 912, MSEI - 18300, ICEX - 1133, MCX - 56415, NCDEX - 1286 | AMFI : ARN-12417 | Research Analyst : INH000000206

Trinity, 226/1, A.J.C. Bose Road, 7th Floor, Kolkata - 700 020, India.

**Investments in securities market are subject to market risks, read all the related documents carefully before investing.