HCL Technologies just released its Q2 FY26 numbers, and investors got plenty of good news to process. Whether you’re tracking your IT stock portfolio, analysing sector trends, or just keeping tabs on India’s tech giants, these results tell an interesting story about where the industry is headed.

The company posted a net profit of ₹4,236 crore, flat compared to last year but up 10% from the previous quarter. Revenue reached ₹31,942 crore, growing 5.2% quarter-on-quarter and 10.7% year-on-year. Operating margin jumped to 17.4%, gaining 116 basis points from last quarter.

These aren’t just numbers, they show how HCL Tech is managing to stay ahead in a tech landscape that’s changing faster than ever.

HCL Technologies is one of India’s big three IT services companies, competing head-to-head with TCS and Infosys for major global clients. The company has built its reputation on delivering digital transformation projects, engineering services, and enterprise software—areas where client relationships often last for decades.

What makes HCL Tech different from its competitors isn’t always obvious from quarterly reports. The company has pushed hard into engineering services and product development, two areas where traditional IT firms usually find it tough to compete. This strategy explains a lot about how their revenue mix is changing and why margins are moving the way they are.

These Q2 numbers came at a time when market expectations were already running high, thanks to better-than-expected results from some competitors. HCL Tech delivered on those expectations, though the real story lies in the details.

| Consolidated Results (₹ cr.) |

Dec 2024 | Mar 2025 | Jun 2025 | Sep 2025 |

| Net Profit | 4,594 | 4,309 | 3,844 | 4,236 |

| Sales | 29,890 | 30,246 | 30,349 | 31,942 |

| EPS in Rs | 16.92 | 15.87 | 14.16 | 15.61 |

That ₹4,236 crore profit number looks flat year-over-year, but there’s more to it. The 10% jump from last quarter shows momentum is building.

Revenue of ₹31,942 crore beat what analysts were expecting, driven mostly by digital services and engineering projects rather than basic IT maintenance work. The EBIT margin hitting 17.4% marks a comeback from earlier quarters when restructuring costs and heavy investments squeezed profits.

Looking at how HCL Technologies makes its money tells a better story than just the overall growth numbers. Digital services grew 15% year-over-year and now make up 42% of services revenue.

Here’s the part that really caught attention: HCL Tech’s AI business crossed $100 million in quarterly revenue. They became the first Indian IT company to report standalone AI revenue at this level. The actual dollar amount matters less than what it shows about client demand for AI services. While most IT firms talk about their AI capabilities, HCL Tech is actually making real money from it.

HCL Tech MD C Vijayakumar reports, “A standout quarter on every front — marked by strong execution, growing demand for our AI-powered solutions, and Advanced AI revenue exceeding $100M this quarter. Our revenue grew 2.4% sequentially in constant currency with a strong recovery of operating margin to 17.5%.”

Brokerages noticed these margin improvements and raised their target prices for HCL Tech shares. Several analysts upgraded their outlook based on both the margin recovery and the accelerating digital business.

New deal wins totalled $2.57 billion in contract value this quarter, up 42% from last quarter and 16% year-over-year.

What’s worth noting is that HCL Tech didn’t win any mega-deals this quarter. Instead, the bookings came from a wide range of clients across the banking, financial services, hi-tech, and engineering sectors.

Different business segments showed different patterns. HCL Software posted recurring revenue of $1.06 billion, growing just 0.6% year-over-year. Meanwhile, digital transformation and engineering services kept pushing growth forward, with management pointing to strong pipelines in banking and hi-tech as future growth drivers.

The fact that there were no mega-deals might worry some people, but it actually shows something positive. When bookings come from many different clients and sectors, it means HCL Tech’s services are valued broadly, not just because of one or two lucky wins.

Management stuck with their FY26 revenue growth forecast of 3-5% year-over-year in constant currency. Among India’s major IT firms, that’s on the higher end of what people expect.

Specifically for services revenue, they’re projecting 4-5% growth year-over-year in constant currency, with operating margins staying in the 17-18% range. That margin forecast suggests management thinks the recent improvements will last, not just be a one-quarter blip.

CEO C. Vijayakumar called Q2 FY26 “a standout quarter” for the company, highlighting strong work in digital and AI transformation. Beyond the typical CEO enthusiasm, the actual numbers back this up.

Management also talked about their workforce plans, particularly their push to rely less on H-1B visas by hiring more people locally in the markets they serve.

HCL Tech announced an interim dividend of ₹12 per share for Q2 FY26. The record date is October 17, with payment scheduled for October 28. This marks their 91st consecutive quarterly dividend, a streak that’s rare in India’s IT sector and shows consistent cash generation.

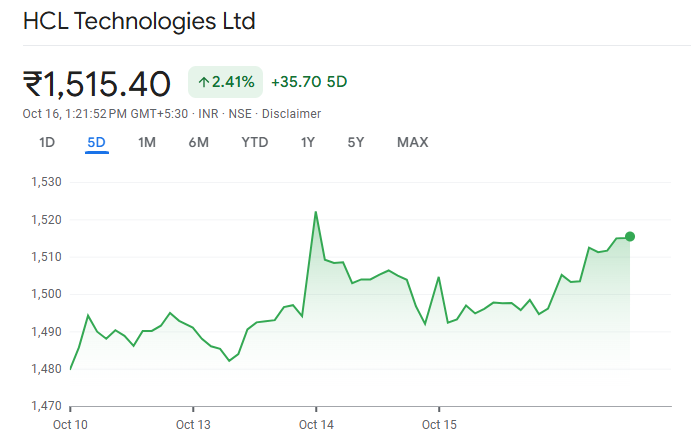

Investors liked what they saw, pushing HCL Tech’s shares up about 2% after the results came out. That gain helped reverse some of the sector-wide decline from earlier this year, when IT stocks dropped on worries about slowing tech spending globally.

Source: Google Finance

The stock is up 2.54% over the past month, though it’s still down nearly 18% compared to a year ago. That annual drop mirrors what’s happening across the entire Indian IT sector, not just HCL Tech specifically.

Even with these strong results, HCL Tech faces real challenges that good quarterly numbers can’t fix. Costs keep rising, especially as they invest in new delivery centers and technology. Restructuring expenses continue as they shift their business toward faster-growing service areas.

Regulatory issues, especially around US immigration and H-1B visa rules, create uncertainty. Their strategy of hiring more locally and setting up nearshore centers should help protect them from visa problems, though making this change takes time and costs money.

Beyond company-specific issues, the whole IT sector faces uncertainty from global politics, clients cutting budgets, and competition from cloud-focused firms and specialized AI service providers.

HCL Tech’s Q2 FY26 results confirm they’re among the sector leaders in growth, managing costs well, and staying innovative.

For investors, employees, and clients, these results show HCL Tech’s operational strength and focus on high-growth areas—even while facing multiple challenges.

The company’s forward-looking approach and track record of execution make it worth watching closely as India’s IT sector moves through its next transformation phase.

Read more: HCL Tech Q2 FY26 Investor Release

Q1: What was HCL Tech’s Q2 FY26 net profit?

₹4,236 crore, flat year-over-year but up 10% quarter-over-quarter.

Q2: What is the interim dividend announced for Q2 FY26?

₹12 per share, marking the 91st consecutive quarterly payout. Record date is October 17, payment on October 28.

Q3: What revenue growth guidance has HCL Tech provided for FY26?

Revenue growth projected at 3-5% year-over-year in constant currency; EBIT margin outlook 17-18%.

Q4: How much revenue is HCL Tech generating from AI and digital services?

Digital services contributed 42% of total revenue; AI business crossed $100 million in quarterly revenue.

Open Free Demat Account!

In just a few minutes, Simply provide some basic personal details, to get started.

About | Research | Pricing | Upcoming IPOs | Blog | Become a Partner | RMS Policy | Privacy Policy

Fund Transfer for Trading | Fund Transfer for DP | Client Back office/DP Login | Partner Login | Buy-Back | Margin Calculation | Re-KYC | Downloads | Platform

CIN - U65921WB1994PLC217071 | SEBI Registration No. INZ000169130 | DP SEBI Reg ID : IN-DP-533-2020 | CDSL : 1234500 | NSDL : IN303591 | Member ID`s : NSE - 08334, BSE - 912, MSEI - 18300, ICEX - 1133, MCX - 56415, NCDEX - 1286 | AMFI : ARN-12417 | Research Analyst : INH000000206

Trinity, 226/1, A.J.C. Bose Road, 7th Floor, Kolkata - 700 020, India.

**Investments in securities market are subject to market risks, read all the related documents carefully before investing.